It has been five years since the Credit CARD Act of 2009 was passed, has it made a positive impact? Is it out of date already? Here’s one reason why it might be.

I am what you’d call a ‘deadbeat’…no really. ‘Deadbeat’ is a term commonly used by credit card companies for those who pay their balance off every month. That means the credit card companies do not make finance charges or fees on my, except I do have an annual maintenance fee. Does that mean the credit card companies make no money on us? Absolutely not! Every time I swipe my card the credit card company is making money by charging the merchant a processing fee.

Last December, I blogged about how I got over $2,000 back from my credit card company. We try to put everything we can on the credit card because of the cash back we get on our Capital One Venture Card. I know of several others who utilize their credit cards to wrack up points or miles. The trick is making sure that it is paid in full each month. My husband and I have gotten into the habit of logging into our accounts each week and making a payment on our credit card so we don’t let our spending get out of control to where we cannot pay it off within the month.

Congress understood that consumers did not understand the terms of our credit card contracts and likely the power of compound interest. For years I have stressed to my students the importance of calculating how much you are paying for something when you borrow the money. I say “if you do not know when you will have the item paid for then you should not be borrowing to buy it”.

Now this can come as a shock right? Have you ever signed mortgages papers and saw how your interest over the life of a 30-year loan was two to three times the amount you were borrowing? It can be hard to swallow, but that’s a good thing.

Time and time again I’ve heard from students they assumed they were doing the ‘right’ thing by making the minimum payment on their credit card. “I got a bill that says to pay $25, I paid it, all must be well.” Not all think this way, but many do fall in the trap.

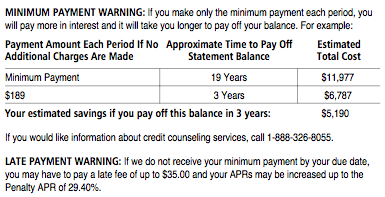

While lecturing about credit to my summer students I mentioned some of the aspects of the Credit CARD Act of 2009, one being the requirement that the credit card companies show on your statement how long it would take to pay off your balance by making the payment and the total, including interest, you would pay. In addition, the credit card companies are required to show you how much you need to pay in order to pay off the balance in three-years (assuming of course you do not charge anymore and your interest rate does not increase). I though about this for a moment and realized I had never see this on my statement?

Was my credit card company out of compliance?

No, because I don’t actually look at my statements. I receive electronic statement notifications, log in each week, review my transactions and pay accordingly. I am a ‘deadbeat’! I never actually look at my credit card statement. In order to view my statement I have to log into my account and download the pdf to look at my statement.

I am not sure how many customers opt to receive electronic statements, as I do, but I’m pretty sure the percentage is pretty high. We live in an electronic age that encourages us to, not only, seek instant information, but also be ‘go paperless’.

Do you agree this regulation might be out of date already? In 2009, electronic statements were very prevalent, why didn’t anyone think to also require these minimum payment calculations show on the home screen when you login?

It would make people think twice to see this right when they login. This comes from my credit card statement, which I finally downloaded and looked at. Why don’t they add a third option “pay in full” pay off now and pay “0” interest?

Would love your feedback!

Melody Bell